How to Prevent Risks with Equity Release Mortgages

Wiki Article

A Comprehensive Guide to Picking the Right Equity Release Mortgages for Your Needs

Selecting the ideal equity Release mortgage is a considerable decision for lots of home owners. It includes recognizing different products and reviewing personal economic requirements. With options like lifetime home loans and home reversion plans, the path can seem complex. Secret factors to consider consist of rates of interest and versatility. As people navigate this landscape, evaluating potential risks and benefits ends up being important. What elements should one focus on to ensure the best result?Understanding Equity Release Mortgages

Equity Release home mortgages provide a monetary remedy for property owners wanting to access the value secured their buildings. Largely designed for individuals aged 55 and over, these home loans enable them to convert component of their home equity into money while remaining to stay in their homes. Homeowners can utilize these funds for different objectives, such as supplementing retirement income, funding home improvements, or covering healthcare costs. The core concept behind equity Release is that the loan is repaid upon the property owner's death or when they relocate right into long-lasting treatment, whereupon the residential property is typically sold to clear up the financial debt. This method allows individuals to appreciate the advantages of their home's value without requiring to move. It is crucial for potential customers to recognize the implications of equity Release, including prospective influence on inheritance and continuous monetary commitments, prior to making a choice.Kinds of Equity Release Products

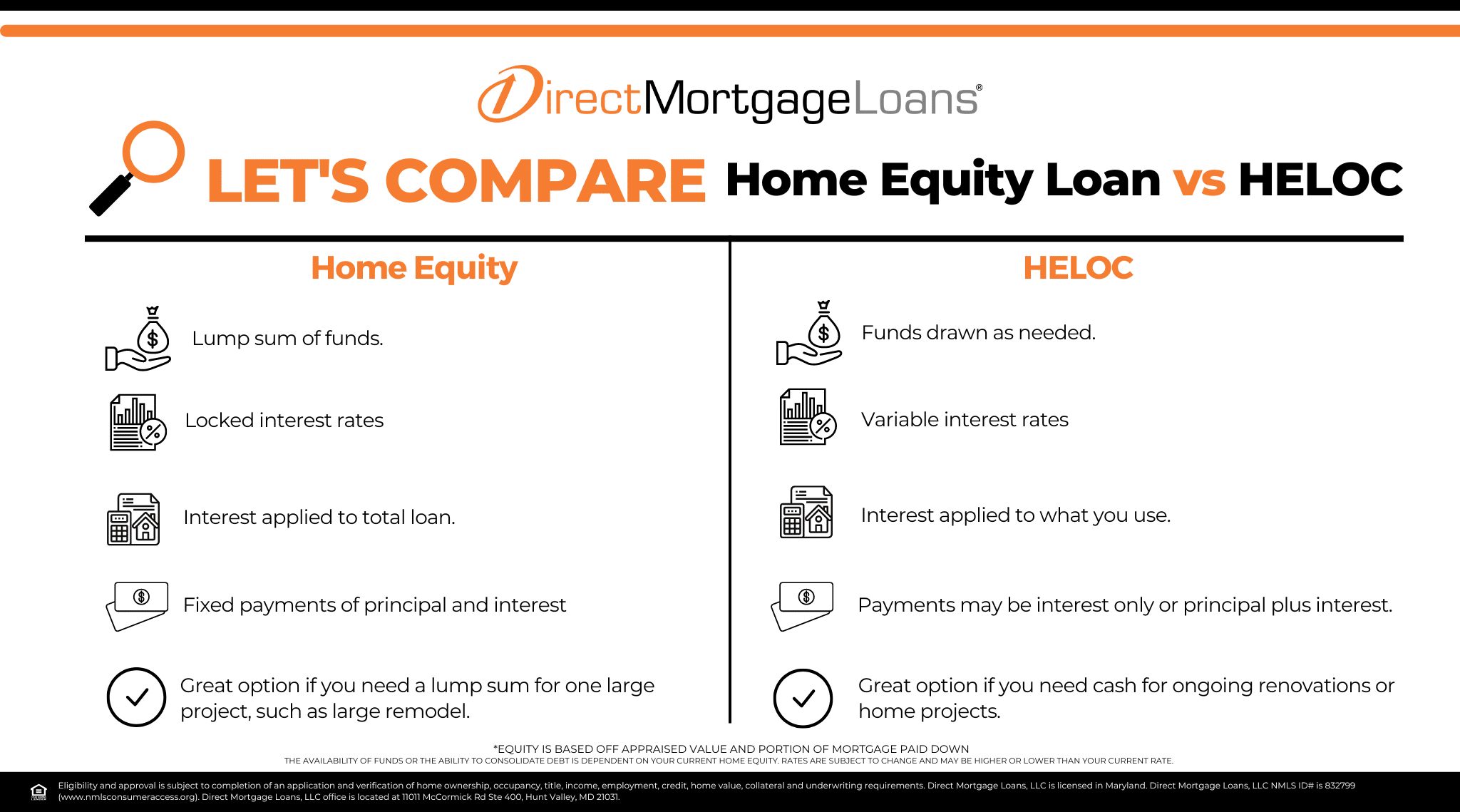

When exploring equity Release items, it is necessary to comprehend the primary types readily available. Lifetime home loans, home reversion plans, and drawdown plans each offer unique functions and advantages. Examining these options can help people in making educated financial choices regarding their residential or commercial property.Life Time Home Loans Explained

Lifetime home mortgages represent among the most usual forms of equity Release products readily available to homeowners in retired life. This kind of home mortgage enables people to obtain against the worth of their home while retaining ownership. Usually, the finance and rate of interest built up are settled when the property owner passes away or relocates right into lasting care. Debtors often have the choice to choose in between set and variable rates of interest, along with whether to make month-to-month settlements or allow the passion roll up. The amount available to borrow typically depends on the home owner's age and building worth. This economic solution can provide retired people with required funds for various needs, including home renovations or additional earnings, while permitting them to continue to be in their homes.Home Reversion Schemes

Drawdown Program Summary

Drawdown strategies represent an adaptable option within the spectrum of equity Release products, enabling home owners to access their residential property's worth as needed. These strategies enable individuals to Release a section of their home equity incrementally, as opposed to obtaining a round figure upfront. This adaptability can be particularly valuable for managing financial resources with time, as customers only pay passion on the quantities they withdraw. Normally, drawdown strategies come with a pre-approved limit, making sure that home owners can access funds when necessary without reapplying. Furthermore, this technique can aid minimize the impact of compounding rate of interest, as less money is borrowed at first. Generally, drawdown strategies deal with those looking for monetary versatility while preserving control over their equity Release journey.Key Elements to Think About

When selecting an equity Release mortgage, numerous vital variables necessitate mindful factor to consider. Rates of interest comparison, the loan-to-value proportion, and the adaptability of functions used can considerably affect the suitability of an item. Examining these aspects will aid people make educated choices that line up with their financial objectives.Rate Of Interest Rates Contrast

Navigating the landscape of equity Release home mortgages needs careful factor to consider of rate of interest, which play an essential duty in figuring out the overall price of the finance. Borrowers should contrast variable and set rates, as dealt with rates supply stability while variable prices can vary based upon market conditions. In addition, the timing of the rate of interest lock-in can considerably impact the overall settlement amount. Possible customers have to also assess the annual percentage price (APR), that includes different costs and costs related to the mortgage. Comprehending the effects of different rate of interest prices will allow people to make enlightened decisions tailored to their economic situation. Ultimately, a detailed analysis of these elements can bring about more beneficial equity Release end results.

Loan-to-Value Proportion

The loan-to-value (LTV) proportion offers as an essential metric in the domain name of equity Release home loans, affecting both qualification and loaning ability. It is calculated by dividing the amount of the funding by the evaluated worth of the property. Generally, a higher LTV ratio indicates a greater risk for lenders, which can lead to stricter lending criteria. Most equity Release items have certain LTV restrictions, commonly figured out by the age of the debtor and the value of the home. LTV ratios generally range from 20% to 60%, relying on these variables. Recognizing the effects of the LTV ratio is important for borrowers, as it straight influences the amount they can access while ensuring they continue to be within risk-free borrowing restrictions.Versatility and Functions

Understanding the adaptability and functions of equity Release home mortgages is vital for borrowers looking for to maximize their economic choices. Different items offer differing levels of adaptability, such as the capability to make partial settlements or the choice to take a swelling sum versus normal withdrawals. Debtors should likewise consider the mobility of the mortgage, which enables them to move it to a brand-new home if they decide to move. Added features like the capacity to consist of member of the family or the option for a no-negative-equity assurance can boost protection and peace of mind. Eventually, reviewing these elements will certainly aid customers More Bonuses choose a plan that aligns with their long-lasting individual circumstances and financial goals.The Application Refine

Just how does one browse the application procedure for equity Release mortgages? The journey begins with examining qualification, which typically requires the applicant to be at the very least 55 years of ages and have a considerable portion of their home. Next, people need to collect necessary paperwork, including proof of building, revenue, and identity valuation.Once prepared, applicants can approach a lending institution or broker concentrating on equity Release. A monetary advisor might additionally supply important guidance, ensuring that all alternatives are considered. Following this, the candidate submits a formal application, that includes an in-depth assessment of their financial scenario visite site and residential property details.The loan provider will after that conduct an assessment, which may involve a home assessment and discussions concerning the applicant's demands and scenarios. The process finishes with a formal offer, permitting the applicant to assess the terms before making a decision. Clear interaction and understanding at each step are necessary for a successful application.

Charges and prices Involved

Many costs and fees are connected with equity Release home mortgages, and potential borrowers ought to know these financial considerations. There may be an application fee, which covers the loan provider's management prices. Additionally, appraisal charges are usually required to evaluate the building's well worth, and these can differ considerably based on the residential or commercial property's dimension and location.Legal charges need to additionally be factored in, as consumers will certainly require a lawyer to browse the lawful facets of the equity Release procedure. Some lending institutions might enforce early repayment charges if the home mortgage is paid off within a details term.It is crucial for consumers look at these guys to completely evaluate all costs linked with an equity Release mortgage, as they can impact the total value of the equity being released. A clear understanding of these costs will enable people to make educated decisionsPossible Dangers and Advantages

Equity Release mortgages feature a range of prices and charges that can influence a consumer's monetary situation. They supply considerable advantages, such as access to funds without the demand to offer the home, permitting debtors to use the cash for retirement, home renovations, or to support member of the family. Nevertheless, potential dangers exist, consisting of the reduction of inheritance for successors, as the car loan quantity plus rate of interest have to be paid back upon the consumer's death or move right into long-term care. Additionally, the home's worth might dislike as expected, causing a bigger financial debt than anticipated. Customers may likewise face restrictions on selling the home or relocating. It is crucial for people to carefully weigh these risks against the benefits to determine if equity Release aligns with their long-term financial objectives. A comprehensive understanding of both aspects is vital for making an informed choice.Inquiries to Ask Prior To Dedicating

When considering an equity Release home mortgage, possible debtors ought to ask themselves several vital inquiries to assure they are making an educated choice. They ought to first review their monetary circumstance, consisting of existing financial debts and future requirements, to determine if equity Release appropriates. It is vital to ask about the total prices included, consisting of charges, rates of interest, and any type of fines for early repayment. Debtors ought to additionally ask exactly how equity Release will certainly impact inheritance, as it might decrease the estate left for successors. Comprehending the regards to the agreement is crucial; as a result, inquiries regarding the adaptability of the strategy, such as the ability to make settlements or take out added funds, should be addressed. Ultimately, possible borrowers ought to take into consideration the reputation of the lending institution and whether independent financial recommendations has actually been sought to ensure all elements are thoroughly recognized.Regularly Asked Inquiries

Can I Choose Just How Much Equity to Release?

Individuals can generally select just how much equity to Release from their home, but the amount may be influenced by aspects such as age, home worth, and lending institution demands - equity release mortgages. Consulting with a financial consultant is a good idea

What Occurs if Building Values Reduction?

If property worths reduce, the equity available for Release diminishes, possibly resulting in a scenario where the impressive mortgage surpasses the residential or commercial property worth. This circumstance may restrict financial choices and impact future planning for home owners.Can I Still Move Home With Equity Release?

The ability to move home with equity Release relies on the particular regards to the equity Release plan. Normally, many plans permit homeowners to transfer their equity Release to a brand-new residential or commercial property, based on authorization.How Does Equity Release Impact My Inheritance?

Equity Release can greatly impact inheritance. By accessing home equity, the general worth of an estate might lower, potentially decreasing what recipients obtain. It's essential for individuals to take into consideration these ramifications when choosing equity Release options.Are There Any Age Limitations for Applicants?

Age limitations for equity Release candidates normally call for people to be a minimum of 55 years of ages (equity release mortgages). Lenders might have added standards, often considering the applicant's financial situation and the residential or commercial property's value during the evaluation processConclusion

In recap, picking the appropriate equity Release home loan needs careful assessment of individual economic conditions and objectives. By comprehending the different product kinds, vital variables, and connected expenses, borrowers can make enlightened choices. Furthermore, recognizing potential threats and benefits is important for long-term economic stability. Seeking independent economic recommendations can even more enhance the decision-making procedure, guaranteeing that the chosen equity Release solution straightens with the homeowner's total monetary strategy and future ambitions. Equity Release home mortgages offer an economic service for homeowners looking to access the worth locked in their properties. Comprehending the flexibility and functions of equity Release home loans is crucial for debtors looking for to maximize their economic options. Some loan providers might impose early settlement charges if the home loan is paid off within a certain term.It is crucial for consumers to thoroughly examine all costs connected with an equity Release home mortgage, as they can impact the general value of the equity being released. The capacity to move home with equity Release depends on the certain terms of the equity Release plan. Seeking independent monetary recommendations can further enhance the decision-making process, making certain that the chosen equity Release option straightens with the homeowner's overall monetary method and future aspirations.Report this wiki page